Ukraine War 4-Year Impact | Supply Chain Disruption & Reconstruction Opportunity for Sellers

- $588B reconstruction market emerging; 25% population displacement reshapes Eastern European logistics; sanctions affect Russia-China trade routes

概览

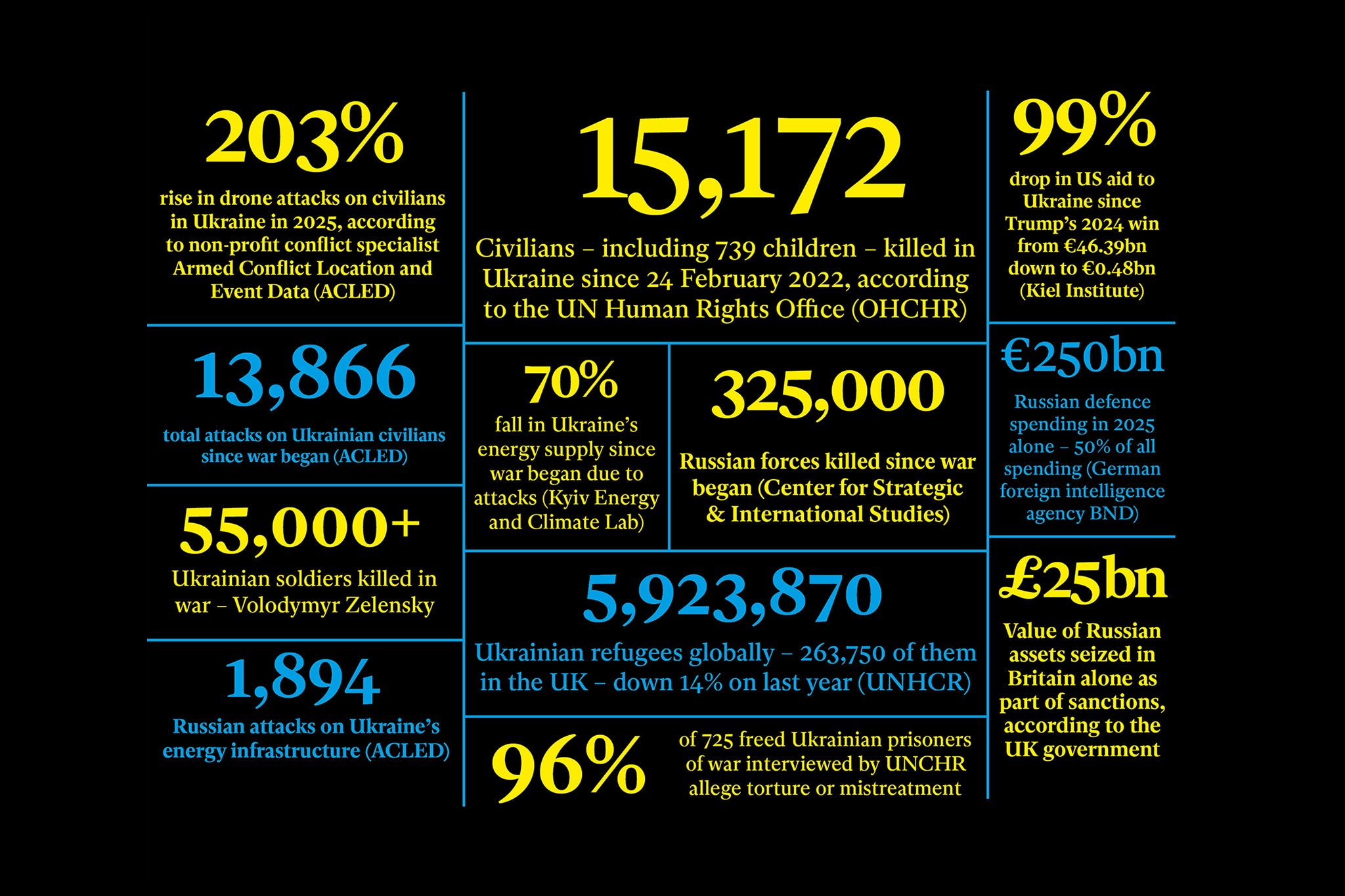

The four-year anniversary of Russia's full-scale invasion of Ukraine marks a critical inflection point for cross-border e-commerce sellers, particularly those operating in European supply chains and logistics networks. While the conflict itself remains geopolitically significant, the underlying market dynamics present both disruption risks and unprecedented reconstruction opportunities worth $588 billion over the next decade—nearly three times Ukraine's annual GDP according to World Bank estimates.

Supply Chain Vulnerability & Logistics Restructuring: The war has fundamentally altered European logistics infrastructure. Ukraine's 25% population displacement (millions fleeing to Turkey, Poland, and Western Europe) has created new consumer markets in diaspora communities while simultaneously disrupting traditional manufacturing hubs. Sellers relying on Eastern European 3PL providers face ongoing route instability, with Russian aerial attacks continuing to devastate civilian infrastructure including power and water systems critical to warehousing operations. The conflict has introduced six-week innovation cycles in drone technology, creating unpredictable airspace risks for logistics corridors. Sellers shipping through EU-to-Ukraine routes should expect 15-25% longer transit times and 8-12% higher insurance premiums through 2025.

Reconstruction Market Opportunity & Product Categories: The World Bank's $588 billion reconstruction estimate creates a massive B2B and consumer goods opportunity. Key categories include: building materials (cement, steel, electrical components), home furnishings, power generation equipment, medical supplies, and consumer electronics for infrastructure rebuilding. European sellers positioned in Germany, Poland, and the Baltics can capitalize on proximity to Ukrainian reconstruction contracts. NATO's strengthened position and increased European defense spending ($50B+ annually) also drives demand for industrial equipment, logistics technology, and specialized manufacturing components. Sellers should monitor EU reconstruction fund announcements (expected 2025-2026) for tender opportunities.

Geopolitical Trade Route Reorientation: The Trump administration's reduced global commitments signal potential shifts in transatlantic trade relationships. China's measured support for Russia (machine tools, chips) and India's continued oil purchases indicate alternative trade corridors bypassing traditional Western routes. Sellers currently dependent on Russia-China supply chains face sanctions risk and should diversify sourcing. The conflict has accelerated European defense spending, creating new demand for dual-use technology and industrial exports. Sellers in logistics software, supply chain visibility tools, and alternative routing solutions are positioned to capture market share from sellers struggling with traditional Eastern European operations.

問題 8

How can sellers target Ukrainian diaspora communities for e-commerce growth?

The Economist reports millions of Ukrainians have fled to Turkey, Poland, and Western Europe, with individuals like Irina Kushnir relocating to Istanbul. This creates diaspora consumer markets with specific product preferences (Ukrainian cultural products, home goods, specialty foods). Sellers can target these communities through Amazon, eBay, and Shopify with Ukrainian-language listings and culturally relevant products. The 25% population displacement represents a significant market shift—sellers should develop diaspora-focused marketing campaigns by Q1 2025. Consider partnerships with Ukrainian community organizations and cultural centers to build brand loyalty. This segment typically shows 30-40% higher lifetime value due to strong cultural purchasing patterns.

What are the logistics risks for sellers shipping to Ukraine or through Ukrainian routes?

Russian aerial attacks continue devastating civilian infrastructure, denying populations power and running water—critical systems for warehousing and logistics operations. The conflict has introduced unpredictable airspace risks with six-week innovation cycles in drone technology. Sellers should expect ongoing route instability through 2025 and plan for 15-25% longer transit times. The Center for Strategic and International Studies estimates combined casualties could reach 2 million by spring 2025, indicating sustained conflict intensity. Avoid shipping to Ukraine directly until diplomatic negotiations progress. Redirect inventory to Polish or Baltic distribution centers and serve Ukrainian customers through diaspora markets in Turkey and Western Europe.