PayPal Takeover Speculation Reshapes Cross-Border Payment Economics for E-Commerce Sellers

- Stock surge 5.74-9.7% signals potential ownership change affecting millions of sellers' transaction fees, settlement speeds, and financing access

/tpg/sources/b455ba7f-7510-49f3-a35f-b0b806962968.jpeg)

概览

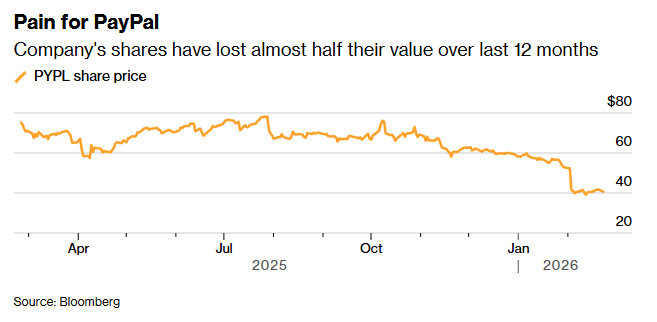

PayPal's potential acquisition represents a critical inflection point for cross-border e-commerce sellers relying on the platform's payment infrastructure. On February 23, 2026, PayPal's stock surged 5.74% (closing at $44.04) following Bloomberg reports of unsolicited takeover interest from at least one major rival or banking peer, with trading volume reaching 75.3 million shares—258% above the three-month average. The company's valuation has compressed dramatically: trading at just 7.7x free cash flow with shares down 44% year-over-year and 86% below all-time highs. Despite this market pessimism, PayPal achieved record revenue and net income levels, indicating operational strength beneath depressed valuations. Multiple suitors are evaluating acquisition scenarios ranging from full company acquisition to selective asset purchases, with PayPal engaging investment banks on strategic options.

For cross-border sellers, this consolidation signals immediate payment processing cost optimization opportunities. PayPal's depressed valuation and potential acquisition by larger financial institutions (competitors or banking peers) could trigger fee restructuring within 6-12 months post-acquisition. Sellers should immediately audit their PayPal transaction costs: standard cross-border rates currently range 3.49-4.99% plus $0.30 per transaction. An acquirer seeking to integrate PayPal into a larger payments ecosystem may rationalize fee structures, potentially offering volume-based discounts (5-15% reductions for sellers processing $50K+ monthly) or bundled services combining payment processing with working capital financing. The broader fintech consolidation trend—evidenced by Adyen's 5.42% decline reflecting investor reassessment of digital payments growth—suggests acquirers will prioritize merchant retention through competitive pricing rather than margin expansion.

Strategic financial implications extend beyond transaction fees to settlement velocity and financing access. PayPal's Seller Protection programs and cross-border payment capabilities serve millions of online merchants globally. An acquisition by a larger financial institution could accelerate settlement timelines from current 1-2 day cycles to same-day or next-day funding, directly improving cash conversion cycles. More significantly, a banking-backed acquirer could unlock invoice financing and purchase order financing products at 1.5-3.5% monthly rates (versus current 4-6% through alternative lenders), enabling sellers to finance inventory growth without traditional bank credit lines. The timing coincides with PayPal's new CEO Enrique Lores (appointed three weeks prior), suggesting management is actively positioning the company for strategic value realization. Sellers should monitor acquisition announcements for fee schedules, settlement terms, and new financing product launches—these typically roll out 90-180 days post-close.

Currency arbitrage and hedging cost optimization represent secondary but material opportunities. PayPal's cross-border payment infrastructure processes transactions across 200+ currencies. A larger acquirer with proprietary FX operations could reduce hedging costs from current 0.5-1.5% spreads to 0.1-0.3%, directly improving margins on international sales. Sellers with significant EUR/GBP/JPY exposure should evaluate whether acquisition-driven FX improvements justify maintaining PayPal as primary processor versus diversifying to Stripe, Adyen, or regional processors. The market's pricing of PayPal "for death" despite strong fundamentals suggests significant upside potential if acquisition discussions materialize—sellers holding PayPal stock or considering equity compensation should monitor deal progress closely.

問題 7

What FX arbitrage opportunities exist from PayPal's potential acquisition?

A larger acquirer with proprietary FX operations could reduce hedging costs from current 0.5-1.5% spreads to 0.1-0.3%, improving margins on international sales by 0.4-1.2%. Sellers with significant EUR/GBP/JPY exposure should calculate current FX costs: $50K monthly EUR sales at 1% spread costs $500/month ($6,000 annually). Post-acquisition FX improvements could save $2,000-4,000 annually. Sellers should request FX rate quotes from potential acquirers during integration planning and lock in favorable rates if acquisition terms improve pricing. Currency-hedging strategies should be reassessed 60 days post-close when new FX terms take effect.

When should sellers expect PayPal fee and service changes post-acquisition?

Typical fintech M&A integration timelines show fee restructuring announcements 60-90 days post-close, with implementation 120-180 days after. PayPal's February 2026 acquisition discussions suggest potential close by Q2-Q3 2026, with fee changes likely by Q3-Q4 2026. Sellers should document current PayPal costs, settlement terms, and financing rates immediately to establish baseline metrics. Prepare fee negotiation strategies and alternative processor migration plans by Q2 2026. Monitor PayPal investor relations for deal announcements and integration timelines—these typically include 30-60 day merchant communication periods before fee changes take effect.